Rural resilience and finance:

As Head of Solutions mapping at the Egypt UNDP Accelerator Lab, a big part of my work is surfacing grassroots narratives and solutions to complex development challenges. In the time between July and September 2022, we leveraged a suite of qualitative research tools including human-centered design and ethnography to examine the notion of rural resilience, through the lens of men and women whose livelihood depends on agriculture, and to understand the position of finance within tools to achieve it.

The tools emerged from the Lab’s desire to understand what was happening in rural settings in terms of financial services and inclusion, and how it’s connected to rural resilience. In Egypt there is currently a heavy emphasis on rural development and financial inclusion. For example, there is a large government project focused on developing the poorest rural areas. However, there is little insight into how financial inclusion and rural resilience are related and through what channels financial tools can support the achievement of both goals.

>> Download Full report HERE

Team:

Marwa Makhlouf

My roles:

Project Management,

Lead Design Researcher,

Visual and Editorial Design.

Background & Research:

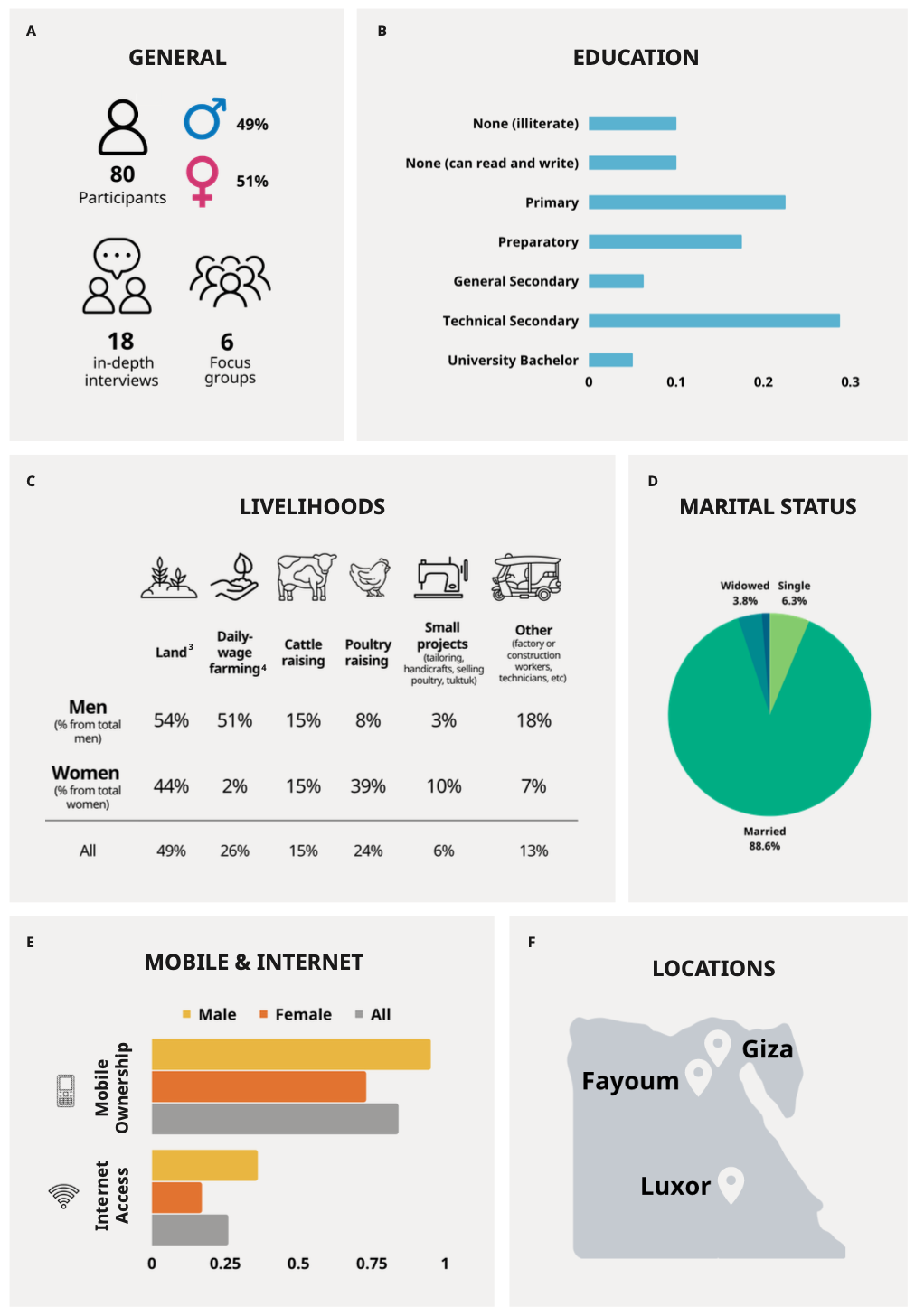

Egypt’s rural population of 57% relies heavily on agriculture, especially small-scale farming, as a livelihood. However, rural Egypt is also confronted with persistent challenges that perpetuate the cycle of poverty and vulnerability. This report outlines the findings and learnings from an exploratory qualitative study conducted between July and September 2022 in 3 villages in different Egyptian governorates; Giza, Fayoum, and Luxor. Following the UNDP Accelerator Lab’s systems thinking approach, the study took a few steps back to examine the notion of rural resilience, through the lens of men and women whose livelihood depends on agriculture, and to understand the position of finance within tools to achieve it.

To this end, the research attempted to understand the following points for the communities in focus:

The livelihood and societal context

The financial behavior and attitude towards formal and non-formal financial institutions

The common and particular hardships encountered by the communities, their impact and the tools used for adaptation and mitigation.

- Systematic review of rural resilience in Kim et al. (2020).

- Sample description

Methodology & tools:

This study mainly adopted a qualitative approach with a participatory direction. The main aim was to use methods that can leave room for exploration, accentuate communities’ voices, and offer deeper explanatory insights into rural resilience and finance. To this end, the following tools were used:

In-depth Interviews (IDI):

In each village 3 IDIs with women and 3 IDIs with men were planned. The IDIs were intended to offer a more private sphere to the participants to be able to prompt them on their financial behavior, individual hardships, community relationships without compromis- ing their privacy to a larger group.

Focus group discussions (FGD):

In each village, 1 FGD with women and 1

FGD with men was planned. The FGDs mainly served in understanding common community-experienced hardships, their impact, how people reacted and adapted to them and whether the participants had ideas for their mitigation in addition to participants’ own interpretation of “resilience”.

- Tools used in IDIs

Findings:

Financial behaviors

During interviews, the research focused on the financial behavior of respondents from sources of income, patterns of expenditure to practices of saving and borrowing in the household. In general, most respondents explained that they do not have budgets for their household finances, nor do they have separate planning for their land expenses (except in cases where land is the main source of income). Monthly income and especially expenditure were hard to estimate mainly due to the precarity of income for those who work on land and construction for daily wages (thus daily unplanned expenditure too), those who receive seasonal income from selling crops and those who have unpredictable medical expenses for a sick child or adult, for example. Nonetheless, the following patterns were inferred regarding financial behavior:

- Financial behaviors

- Personas 4 out of 6

- Land and non-land related hardships

Hardships

Experienced hardships and challenges in the previous 3 years were discussed at length during focus groups and to a lesser degree during interviews. The goal was to understand the most frequent intersecting hardships among the men and women on a community and individual levels, their impact and the adaptation techniques used (financial and non-financial). Afterwards, ideas for mitigation were also prompted whether as attainable or unattainable solutions. By reconciling themes from adaptation and mitigation techniques in addition to participants’ own definitions, contextual elements of resilience can be put together while highlighting the role of financial tools in the rural hardship-resilience nexus.

Resilience

Resilience emerged in multiple forms throughout the interviews and FGDs. Participants were asked directly on how they define resilience; what would a person need to be resilient in their community? What does it mean to be able to overcome a challenge and remain strong afterwards? As resilience is a multi-faceted concept, it presented itself through the different layers, almost similarly for both men and women. It’s important to highlight though that those elements do not include basic rights such as health, education, and infrastructure. Moreover, they may vary in their relevance and effectiveness depending on the magnitude, duration and nature of the shock/hardship.

- Voices on resilience & aspirations

Learnings:

Leveraging subsistence farming for food security: pressures on smallholder farming have implication on the levels of nutrition and food security

Diversifying Livelihoods and expanding into non-farm economies: efficiency of diversifying livelihoods will depend on their value and productivity, additionally they should not replace the creation of stable non-farm opportunities

Strengthening social protection: the combination of risks and precarious livelihoods that rural communities suffer from make the availability of just and inclusive social protection programmes imperative

Accounting for the psychological and community elements: policy and programming for rural development should not neglect the psychological and community dimensions in design, monitoring and evaluation.

Mobilizing agricultural extension services and cooperation among farmers: it is necessary to mobilize knowledge, technological and energy farmer-centric solutions while encouraging and consolidating cooperative modalities among farmers

Designing tailored and meaningful financial services: utilizing the broad range of financial products; credit, savings, and insurance alongside meaningful financial literacy programmes.